Business restructuring

Business restructuring is a purposeful change in the structure of a company that creates an opportunity for a business to successfully develop and achieve certain goals, taking into account the influence of external and internal processes (factors). After all, any change in market conditions, as well as the modification of the business itself, requires an adequate transformation of the management structure and certain restructuring actions.

As practice shows, one of the reasons why companies seek restructuring is the low efficiency of their activities, which can be expressed in negative or unsatisfactory financial performance, the growth of receivables or payables, the emergence of a potential risk of loss of assets or control over the business.

"The first rule of business is to protect your investment"

Banker's Etiquette, 1775

Based on this rule, we consider it appropriate to offer you the opportunity to protect your business by restructuring it.

Business restructuring will help you:

build reliable asset protection

ensure control and protection of corporate rights

optimize the movement of goods / services and finances, taking into account the tax and financial policy of the state (states)

effectively control and use internal and external financial flows

increase the transparency of the company's activities (which is important when working with foreign partners and banks)

timely and effectively control relations with counterparties

create effective protection against unscrupulous counterparties

optimize the tax burden

We conditionally divide restructuring into two types:

Operational (short-term) - the solution of the situation that has arisen, requiring the adoption of the right measures in a short period of time.

Strategic (long-term) - building a business model taking into account a large number of factors.

Each of the above types may include:

- financial restructuring;

- restructuring of the company's assets;

- restructuring of corporate rights.

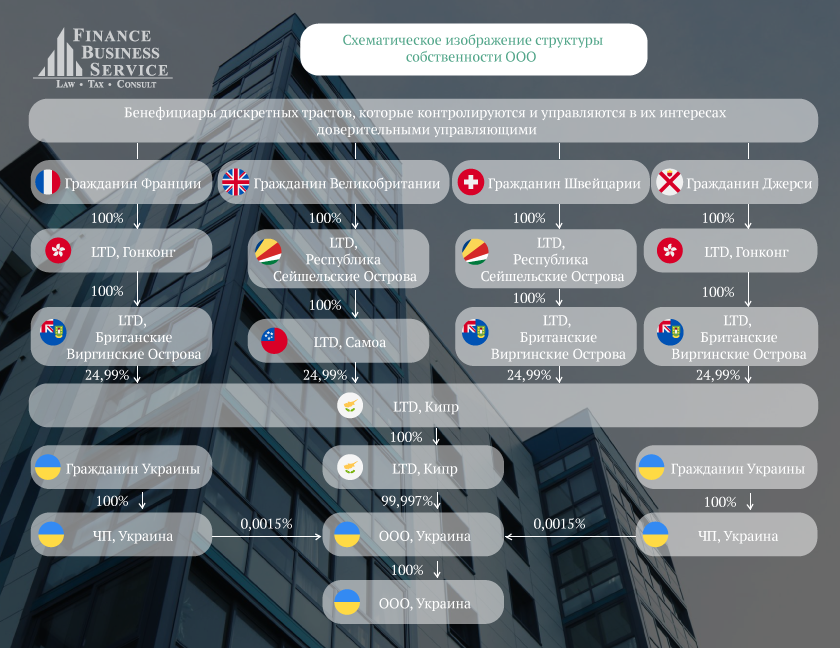

Services offered as part of business restructuring, using foreign companies:

- Protecting the property interests of business owners and building an effective system of legal control;

- Building an effective structure of the company (group of companies) in accordance with the development strategy;

- Reducing the likelihood of bankruptcy;

- Freeing the business from illiquid assets or keeping valuable assets;

- Legal support of business security (protection against hostile takeover);

- Optimization of business processes;

- Optimization of taxation and financial flows.

The result of the restructuring is to increase the stability, profitability and value of the business.